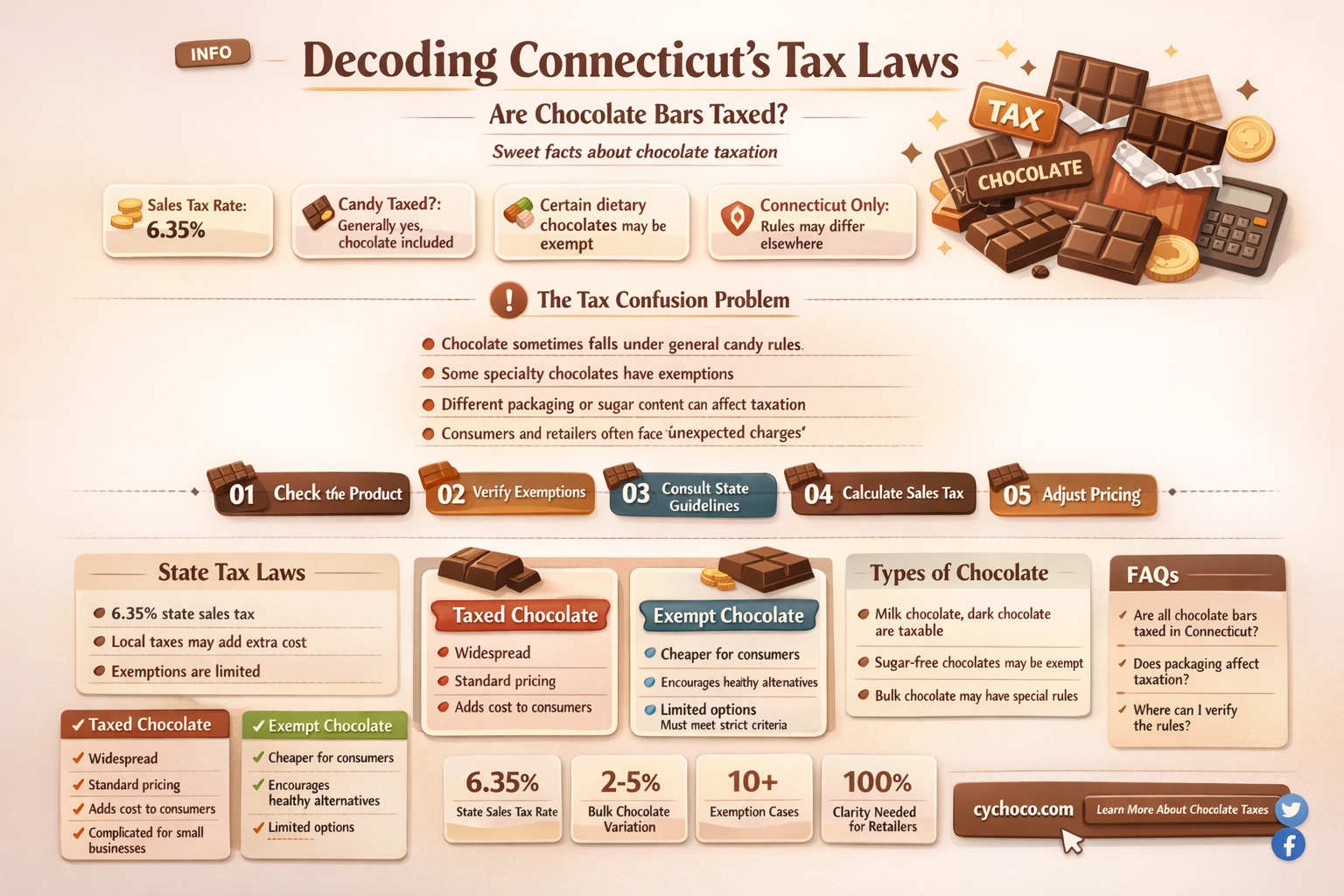

Chocolate bars, as a popular confectionery item, are subject to taxation in many regions, including Connecticut. The taxation of chocolate bars in Connecticut is part of the state's broader sales tax policy, which applies to various goods and services sold within its jurisdiction. Understanding the tax implications for chocolate bars involves examining the state's tax codes and regulations, as well as considering any potential exemptions or special provisions that might apply to certain types of chocolate products. This information is crucial for businesses involved in the sale of chocolate bars, as well as for consumers who are interested in the tax rates applied to their purchases.

| Characteristics | Values |

|---|---|

| Product Type | Chocolate bar |

| Tax Category | Food item |

| State | Connecticut (CT) |

| Tax Rate | Varies (dependent on local tax policies) |

| Tax Applicability | Subject to state and local sales tax |

| Exemptions | None (generally taxable) |

| Additional Fees | None (only sales tax applies) |

Explore related products

What You'll Learn

- Tax Classification: Determining if chocolate bars are taxed as food or candy in Connecticut

- Sales Tax Rate: Identifying the specific sales tax rate applied to chocolate bars in Connecticut

- Exceptions: Exploring any tax exemptions or special rules for certain types of chocolate bars

- Historical Changes: Reviewing past changes in tax laws regarding chocolate bars in Connecticut

- Comparison: Comparing Connecticut's chocolate bar tax policies with those of neighboring states

![]()

Tax Classification: Determining if chocolate bars are taxed as food or candy in Connecticut

In Connecticut, the tax classification of chocolate bars hinges on a nuanced distinction between food and candy. This classification impacts both consumers and retailers, influencing the final price paid at the checkout and the tax liabilities of businesses. To determine whether a chocolate bar is taxed as food or candy, one must consider the ingredients, preparation methods, and intended use of the product.

Food items, including chocolate bars, are generally exempt from sales tax in Connecticut if they meet specific criteria. According to the Connecticut Department of Revenue Services, food means any substance or mixture of substances intended for human consumption, including beverages, but does not include candy. Chocolate bars, when marketed and sold as food items, typically fall under this exemption. This is especially true for dark chocolate, which is often perceived as a healthier alternative due to its higher cocoa content and lower sugar levels.

On the other hand, candy is subject to sales tax in Connecticut. Candy is defined as any sweet, edible confectionery, including chocolates, caramels, and other similar items. The key distinction here is the sugar content and the form in which the chocolate is sold. Milk chocolate and white chocolate, which contain higher sugar levels and are often combined with other sweet ingredients, are more likely to be classified as candy. Additionally, chocolate bars that are marketed and sold in a manner similar to candy, such as those with colorful wrappers and playful branding, may also be subject to sales tax.

Retailers play a crucial role in determining the tax classification of chocolate bars. They must carefully review the product labels, packaging, and marketing materials to ensure that they are applying the correct tax rate. Failure to do so could result in underpayment of taxes, leading to potential penalties and fines. Consumers, while not directly responsible for tax classification, should be aware of these distinctions as they can impact the overall cost of their purchases.

In conclusion, the tax classification of chocolate bars in Connecticut is a complex issue that requires careful consideration of various factors. By understanding the differences between food and candy, retailers and consumers can navigate the tax landscape more effectively, ensuring compliance with state regulations and making informed purchasing decisions.

Creative Ways to Use Hershey's Chocolate Bars in Delicious Recipes

You may want to see also

Explore related products

![]()

Sales Tax Rate: Identifying the specific sales tax rate applied to chocolate bars in Connecticut

To determine the specific sales tax rate applied to chocolate bars in Connecticut, one must first understand the state's tax structure. Connecticut imposes a statewide sales tax, which is currently set at 6.35%. However, local jurisdictions within the state may also levy additional sales taxes, which can vary by town or city.

In the case of chocolate bars, they are generally considered taxable items under Connecticut law. This means that the statewide sales tax of 6.35% would apply to the purchase of chocolate bars. However, depending on the specific location within the state where the chocolate bars are purchased, there may be additional local sales taxes that could increase the overall tax rate.

For example, if a consumer purchases chocolate bars in the city of Hartford, they would pay the statewide sales tax of 6.35%, plus an additional local sales tax of 1%, for a total tax rate of 7.35%. On the other hand, if the same consumer purchases chocolate bars in the town of Greenwich, they would only pay the statewide sales tax of 6.35%, as Greenwich does not impose a local sales tax.

It is important to note that the sales tax rate can change over time, as both state and local governments have the authority to adjust their tax rates. Therefore, it is always a good idea to check the current sales tax rates before making a purchase.

In conclusion, the specific sales tax rate applied to chocolate bars in Connecticut depends on the location within the state where the purchase is made. The statewide sales tax rate is 6.35%, but additional local sales taxes may apply, resulting in a higher overall tax rate in some areas.

Mastering Cocoa: A Guide to Replacing Bar Chocolate in Recipes

You may want to see also

Explore related products

![]()

Exceptions: Exploring any tax exemptions or special rules for certain types of chocolate bars

Connecticut's tax code includes specific exemptions and special rules for certain types of chocolate bars. For instance, chocolate bars that are classified as "candy" are subject to a different tax rate compared to those classified as "food." This distinction is crucial for manufacturers and retailers to understand, as it directly impacts pricing and tax collection.

One notable exception is the tax exemption for chocolate bars that are part of a "gift basket." According to Connecticut tax law, gift baskets that contain a variety of items, including chocolate bars, are exempt from sales tax if the total value of the basket does not exceed $50. This exemption is often utilized by businesses that create and sell gift baskets, as it allows them to offer a tax-free option to customers.

Another special rule applies to chocolate bars that are sold at fundraising events. If the chocolate bars are being sold as part of a charitable fundraiser, they may be exempt from sales tax. However, this exemption only applies if the fundraiser is registered with the Connecticut Department of Revenue Services and meets certain criteria.

Additionally, chocolate bars that are part of a "food assistance program" are also exempt from sales tax. This includes programs such as the Supplemental Nutrition Assistance Program (SNAP) and the Women, Infants, and Children (WIC) program. Retailers must ensure that they are properly authorized to accept these benefits and that they are not charging sales tax on eligible items.

In conclusion, while chocolate bars are generally subject to sales tax in Connecticut, there are several exceptions and special rules that apply. Understanding these nuances is essential for businesses and consumers alike, as it can impact the final cost of the product and compliance with tax laws.

Creative Christmas Chocolate Wrapping: Easy DIY Ideas for Festive Gifts

You may want to see also

Explore related products

![]()

Historical Changes: Reviewing past changes in tax laws regarding chocolate bars in Connecticut

Connecticut's tax laws have undergone several changes over the years, impacting various industries, including the confectionery sector. One significant shift occurred in 2001 when the state introduced a sales tax on certain food items, including chocolate bars. Prior to this, chocolate bars were exempt from sales tax, much like other grocery items. The introduction of this tax was part of a broader effort to increase state revenue and address budget deficits.

In 2004, there was another notable change when the state legislature amended the sales tax laws to exempt certain food items, including chocolate bars, from the sales tax. This move was largely influenced by the lobbying efforts of the confectionery industry and consumer advocacy groups who argued that taxing food items disproportionately affected low-income households.

However, in 2009, the state once again reinstated the sales tax on chocolate bars and other confectionery items as part of a package of tax increases aimed at addressing another budget crisis. This change was met with resistance from the confectionery industry and consumers alike, who argued that it would lead to higher prices and reduced sales.

The most recent change occurred in 2018 when the state legislature passed a bill exempting chocolate bars and other food items from the sales tax. This move was part of a larger effort to reduce the tax burden on consumers and stimulate economic growth. Under the current law, chocolate bars are exempt from sales tax in Connecticut, much like other grocery items.

These historical changes in tax laws regarding chocolate bars in Connecticut highlight the complex and often contentious nature of tax policy. They also underscore the importance of understanding the specific tax laws that apply to different industries and consumer goods.

Is Kit Kat a Chocolate Bar? Unwrapping the Sweet Debate

You may want to see also

Explore related products

![]()

Comparison: Comparing Connecticut's chocolate bar tax policies with those of neighboring states

Connecticut's chocolate bar tax policies stand out in the New England region. While the state does not impose a specific tax on chocolate bars, it does have a general sales tax of 6.35% that applies to most retail sales, including confectionery items. This places Connecticut in a unique position compared to its neighboring states, which have varying approaches to taxing chocolate and other sweets.

In Massachusetts, for instance, chocolate bars are subject to the state's general sales tax of 6.25%. However, Massachusetts also has a separate tax on certain types of candy, including chocolate, at a rate of 3%. This additional tax is known as the "candy tax" and applies to items that are not considered "nutritious." Connecticut, on the other hand, does not have such a specific tax on candy.

New York State has a more complex tax structure when it comes to chocolate bars. The state's general sales tax is 8.875%, but local governments can add their own sales taxes, bringing the total to as high as 14.375% in some areas. Additionally, New York has a tax on certain types of candy, including chocolate, at a rate of 4%. This tax is applied in addition to the general sales tax.

Rhode Island and New Jersey both have a general sales tax that applies to chocolate bars, but neither state has a specific tax on candy. Rhode Island's sales tax is 7%, while New Jersey's is 6.625%. In both states, chocolate bars are taxed at the same rate as other retail items.

When comparing Connecticut's chocolate bar tax policies with those of its neighboring states, it becomes clear that Connecticut has a relatively straightforward approach. The state's general sales tax applies to chocolate bars, but there are no additional taxes on candy or specific types of confectionery items. This simplicity may make it easier for consumers and retailers to understand the tax implications of purchasing chocolate bars in Connecticut.

In conclusion, while Connecticut does not have a specific tax on chocolate bars, its general sales tax of 6.35% applies to most retail sales, including confectionery items. This places Connecticut in a unique position compared to its neighboring states, which have varying approaches to taxing chocolate and other sweets. Understanding these differences can help consumers and retailers navigate the complex tax landscape of the region.

Unwrapping the Mystery: Is a Chocolate Bar a Noun?

You may want to see also

Frequently asked questions

Yes, chocolate candy is subject to sales tax in Connecticut. The state has a general sales tax that applies to most retail sales, including candy.

The sales tax rate for chocolate bars in Connecticut is 6.35%. This is the current statewide sales tax rate that applies to most taxable items, including chocolate bars.

There are no specific exemptions or special rules for taxing chocolate in Connecticut. Chocolate is taxed at the same rate as other candy and most other retail items in the state.